A prior blog post discussed the legal issues relating to the sale of a business or professional practice. One issue mentioned in that article was that of a non-compete clause. This blog post will discuss that issue in further detail as it applies to commercial leasing.

A prior blog post discussed the legal issues relating to the sale of a business or professional practice. One issue mentioned in that article was that of a non-compete clause. This blog post will discuss that issue in further detail as it applies to commercial leasing.

As a great deal of commercial space in the New York metropolitan area involves shopping centers and strip malls in which the stores are in close proximity to each other, a non-compete clause may be essential for a tenant. A non-compete clause in a commercial lease involves an agreement between the landlord and the potential tenant that the landlord will not rent space to a competitor of the tenant, or to a business that draws the same customers who may choose to do business with one tenant as opposed to another. A non-compete clause also comprises the tenant’s promise not to engage in particular business activities. For example, if the tenant sells office supplies, then the tenant may ask for a clause in their commercial lease by which the landlord is prohibited from renting any space in the same shopping center to another store that sells office supplies. In subsequent leases with new tenants, the landlord needs to include the prohibition from selling office supplies so that new tenants do not violate the landlord’s promise to the office supply tenant.

Of course, it is essential that such a clause be drafted with specificity and contain language sufficient to make it clear which competitors, specific activity and types of businesses are prohibited. For example, using the office supply example above, a non-compete clause must be very specific in the types of sales that are prohibited. Many establishments such as grocery stores and drugstores sell items such as writing implements and stationery, even though it is not their primary business. A non-compete clause should be crafted for the specific inventory of the store in question while also providing the business with opportunity for growth and change in inventory as needed.

In

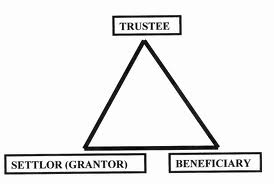

In  Trusts provide a valuable tool in estate planning because they serve the purposes of preserving assets, protecting intended beneficiaries, and potentially saving or eliminating estate taxes. A trust is a legal document that conveys a “corpus”, or body of assets, from the settlor (the person who creates the trust and owns to assets) to a trustee (the individual or corporate entity with the responsibility of holding the assets) for the benefit of the beneficiary (the person who will ultimately receive the proceeds of the trust). A charitable organization may also be the beneficiary of a trust.

Trusts provide a valuable tool in estate planning because they serve the purposes of preserving assets, protecting intended beneficiaries, and potentially saving or eliminating estate taxes. A trust is a legal document that conveys a “corpus”, or body of assets, from the settlor (the person who creates the trust and owns to assets) to a trustee (the individual or corporate entity with the responsibility of holding the assets) for the benefit of the beneficiary (the person who will ultimately receive the proceeds of the trust). A charitable organization may also be the beneficiary of a trust.

Some of our

Some of our  Some of our firm’s clients are in the business of purchasing notes and mortgages encumbering properties which are being foreclosed. This blog post will discuss the legal necessities behind such transactions. Careful planning, as well as consultation with legal counsel, can ensure that such acquisitions comply with all legal requirements and ensure that the purchaser obtains marketable title so that properties so acquired can be resold expeditiously if desired.

Some of our firm’s clients are in the business of purchasing notes and mortgages encumbering properties which are being foreclosed. This blog post will discuss the legal necessities behind such transactions. Careful planning, as well as consultation with legal counsel, can ensure that such acquisitions comply with all legal requirements and ensure that the purchaser obtains marketable title so that properties so acquired can be resold expeditiously if desired.  An article in

An article in  Regional news outlets in the New York metropolitan area recently reported on

Regional news outlets in the New York metropolitan area recently reported on